UAM (Urban Air Mobility) is talked up to become a disrupter of urban mobility.

Billions and Billions of USD are invested and being invested developing electric aircrafts able to takeoff and land vertically and a wast amount of capital is being invested into its needed infrastructure based on a predicted revenue of Billions and Billions.

But are many developers and investors investing their time, livelihood, effort and capital into a futuristic scenario based of todays or based on tomorrows traffic and needs ?

By: John Martin Winther Andersen

UAM, Urban Air Mobility, has been said to become a disrupter of Urban transportation by elevating a lot of the urban traffic from todays congested streets into a mostly non-utilized lower airspace that in comparison has a lot of empty space to share.

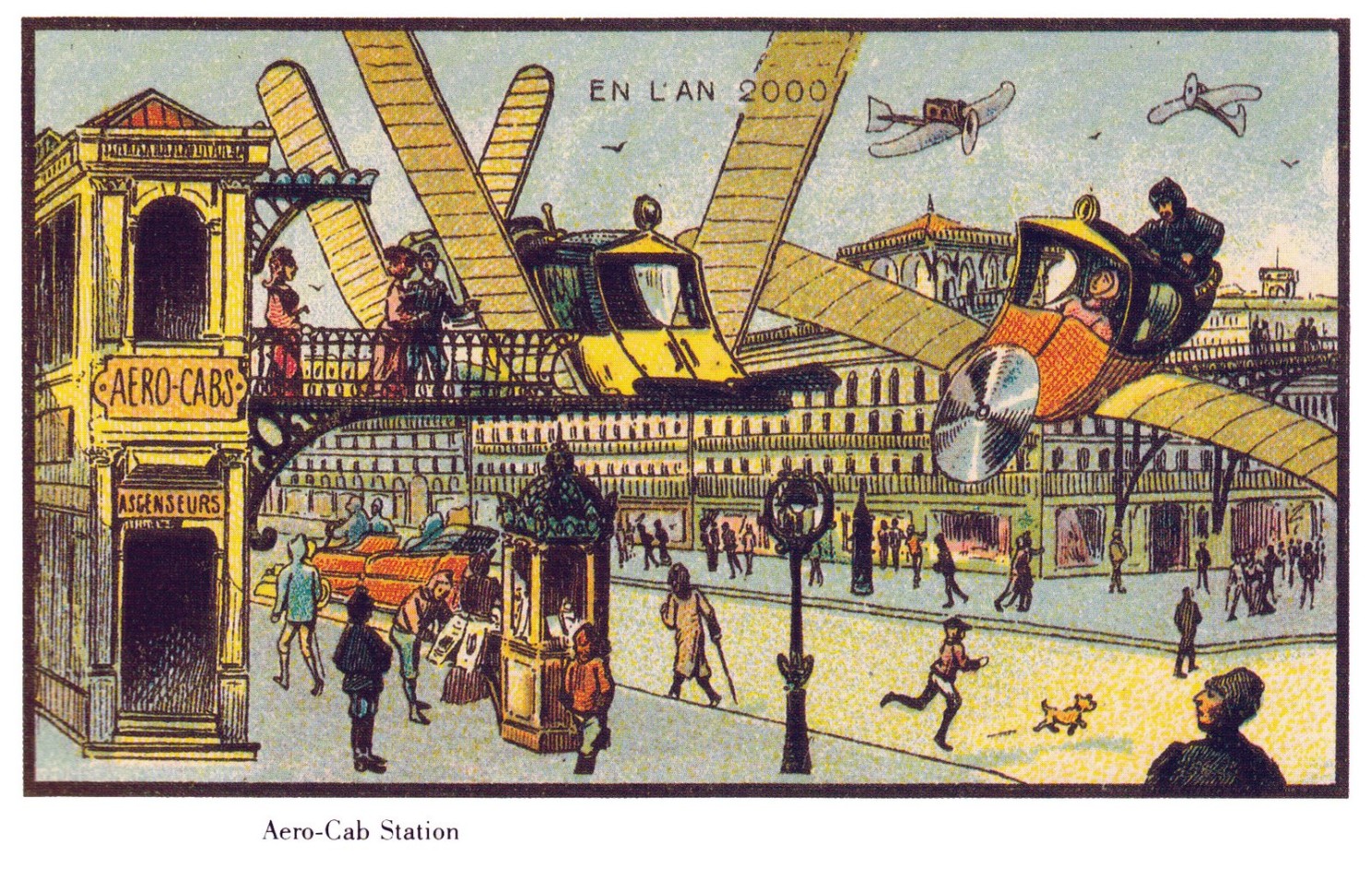

History of AirTaxi usage

Several developers, opinion makers, influencers etc. believe and describe UAM as a novel idea. It really isn't ... wanting to move a lot of traffic from the ground up into the air for a faster mode of travel is no new idea.

The idea has been brewing with us humans for over a century, for example the illustrations from the L'An 2000 series of how people in the early 1900 envisioned a year 2000 future.

Igor Sikorsky envisioned in 1943 a future of urban usage of individual VTOL (Vertical TakeOff and Landing) aircraft for the average citizen.

Bell Helicopters tried in the 70's to "sell" the usage of their light Bell 206 helicopter on a daily basis for businesses in The Greater Los Angeles, though today we can conclude that neither of these ideas never materialized into a scalable business case.

Looking at New York it is pretty much the same story. Scheduled cost competitive but subsidized helicopter routes did take place in New York (and Los Angeles & San Fransisco) in the 50-70's, until a tragic accident happened on the roof of Pan Am high-rise building due to cost-cutting poor operational standards and shortly after the subsidization for this UAM service was removed, making UAM by helicopter to costly and to problematic to sustain a business.

Later Trump Air tried a similarly setup with scheduled helicopters and as late as 2006-09 US Helicopter tried essentially the same type of setup. All attempts was cost-wise limited to the few or very few, not seamless enough to use and therefore all business cases has ultimately failed.

Add Digitization

Add the age of digitization to previous centuries of helicopter AirTaxi business cases, and we have the foundation of for example BLADE in 2014, though not owning nor operating any aircrafts themselves but by utilizing a bespoke UBER-like booking platform incl. crowd sourcing out empty seats that the customer did not want, to lower the cost even further per flight for everyone, i.e. ride-sharing. Prices dropped significantly compared to the past and in a place like New York where traffic across the city can take hours during rush hours, for those who can afford the service it has become a great tool to save time.

Though like this known travel reviewer demonstrate in the video above, USD 150 after discount for a short helicopter ride across New York might be a fair and payable price for a one-time visitor or for the few and wealthy, but not for the masses and their everyday need to commute across the city, such a cost is simply far out of reach for the masses daily budget and their income level. And it is the masses daily commute in the major cities that is needed, to be able to scale up this business case to sustain the projected thousands upon thousands of electric aircrafts (eVTOL's) used in the UAM sector.

Electrifying UAM

Beside the environmental nuisance of noise and emissions, the cost problem has been promised and envisioned to be solved by electrifying the VTOL aircrafts (i.e. eVTOL) and ultimately making the aircrafts autonomous in a future to come ... though time will tell if that autonomous future is a near or distant future.

First time we saw predictions and comparisons of prices with other means of land-based transportation, was from the Uber Elevate 2016 report, as shown below.

Source: Uber Elevate 2016

Source: Uber Elevate 2016

In 2016 UBER estimated that UAM will be price competitive to car ownership not in a near term future but in a long term future of $ 0.40 on average per seat-mile, compared with owning a car in the US of $ 0.73 per seat-mile. What UBER mean of "long-term" is not defined by UBER, but it seems reasonable if we define long-term as +10 years after initial launch of this eVTOL service, so in the late 30's. Keep this in mind for later in this article what to happen in the next decade 30's) ...

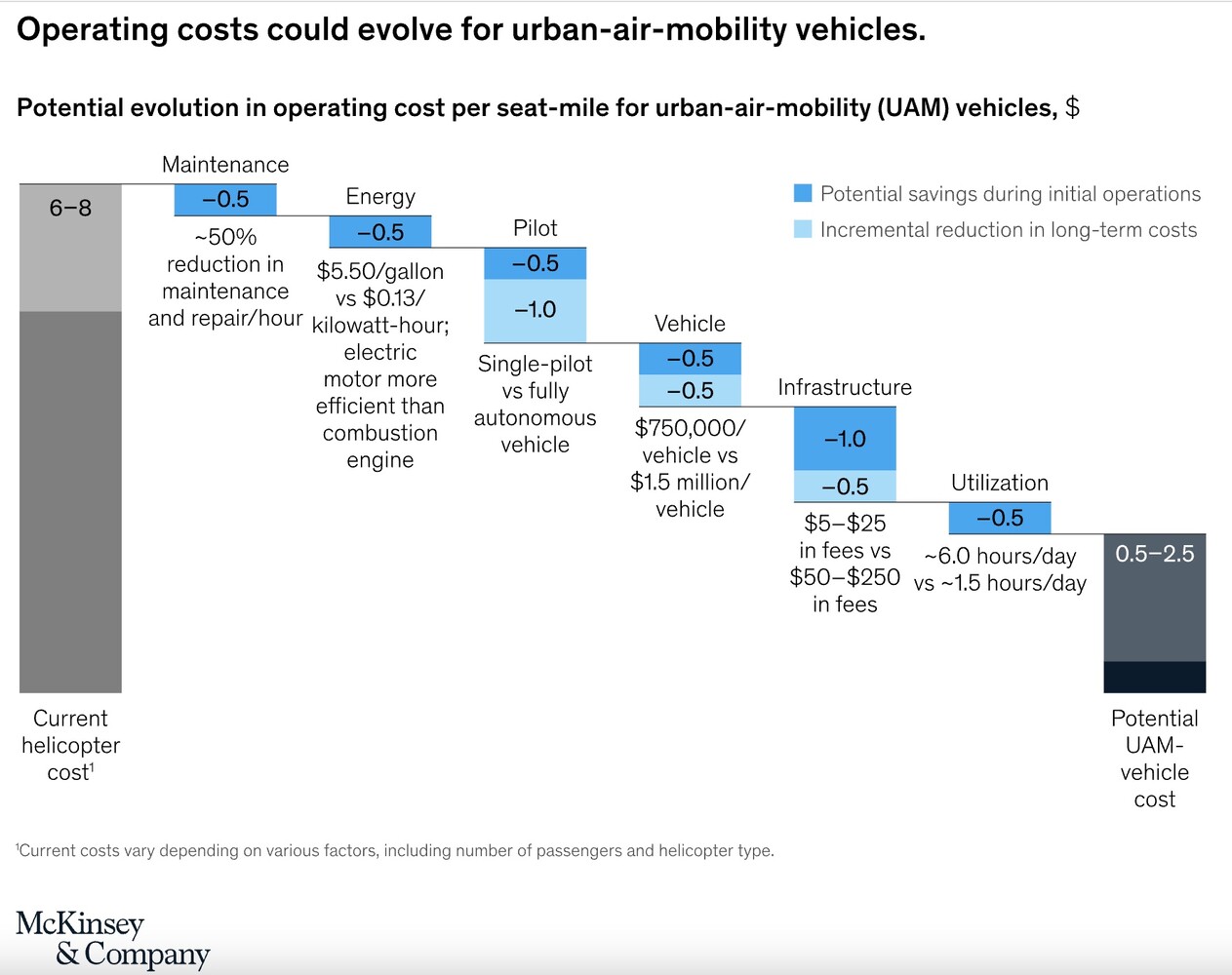

McKinsey & Company published similarly potential cost of operating eVTOL back in their 2020 report, showing the below overview of a potential as low as $ 0.50 per seat-mile.

Source: McKinsey & Company

Source: McKinsey & Company

Note: The UBER and McKinsey numbers above are for the US market. Due to different pricing, incentives and taxation of car ownership in each country, any conclusions on UBER's and McKinsey comparison outside the US should take into account each country differences when comparing with car ownership.

The manufacturers numbers vs. reality

How does these predictions from for example UBER and McKinsey & Company hold up against the leading UAM developers and soon to be manufacturers own numbers ?

In 2021 Joby Aviation announced an initial cost per seat-mile of $ 3.0 in 2026 at just shy of 60% load factor. Archer sets their aircraft at $ 3.30, Lilium at $ 2.35 at 75% load factor and EVE at $ 3.88 per seat-mile, so a bit higher than the cost of initial UAM services projected by UBER in 2016 and McKinsey & Company in 2020.

According to U.S. Department of Transportation and UBER's 2016 chart above, it cost approx. $ 0.72 per seat-mile to use a new private car in the US. And that doesn't count for those households that often for economical reasons has to settle for a cheaper used car to get to work, drive kids to school, grocery shopping etc., who all are a part of the masses they need to use at least to some level their UAM services to scale up their business.

In Europe despite car ownership is often a bit more expensive than in the US, for example in Denmark it cost on average $ 0.95 per seat-mile, it shows the same picture as in the US. There is a huge price gap between driving a private car vs. using UAM services for the larger part of the citizens. Add to the UAM service the need of getting to/from the UAM landing location because they are not going to pick their passenger up nor land at the individual address anyone needs to go to, i.e. The First & Last Milage issue, add to that the need AND cost of some sort of land-based public transportation, taxi or UBER ride.

The average salary in the US is approx. $ 60.000 per year, a salary level that includes those with a Bachelor's Degree. If one was to commute just 25 miles to and from work by UAM five days a week 50 weeks per year, the total cost of the UAM service alone based on the leading eVTOL developers estimate will range from $ 28.000 - 48.000 per year. No Police Officer, no Nurse, no Account Manager, no Engineer, no Store Manager, no Teacher, no Any One holding a normal average paid job i.e. The Masses can afford such cost of commute on a daily basis that UAM has budget with to start with, from where they need to scale up from, to make promise of the production of the thousands upon thousands of eVTOL aircrafts used for UAM. For the first many years services with these leading eVTOL's brands will be only for the few and wealthy, where some of them already use helicopters for the same purpose in the larger metropolises.

As this opinion pease "There Will Be Blood: Dissecting eVTOL Business Models" from Kevin Michaels from 2022, ".. If there is such pent-up demand for this service, why isn’t the world covered with R44 air taxis ..". It is a good question. The R44 is a helicopter type that privately run cost from $ 1.85 per seat-mile in the US all the way up to approx. $ 7.00 per seat-mile commercially in for example Denmark, both at 60% load factor and at merely only 10-20% of the hours annually that the leading eVTOL manufacturers has based their economically assessments on.

Yes, the leading eVTOL developers often compare their multi-engine eVTOL with the cost of a multi-engine helicopter and that for sure makes their numbers look much better, because multi-engine helicopters are 3-4x more expensive to fly than a single engine light piston or light turbine helicopter like the R44 and R66, but what does it matter if the single-engine helicopter is allowed to fly the task as they intend their multi-engine eVTOL shall take over. The customer usually don't care, they and especially the masses that is much MUCH more conscious to get the most bang for their bucks, will pick the single-engine helicopter just like several of the helicopters BLADE book today for their customers out of New York Manhattan Heliport are.

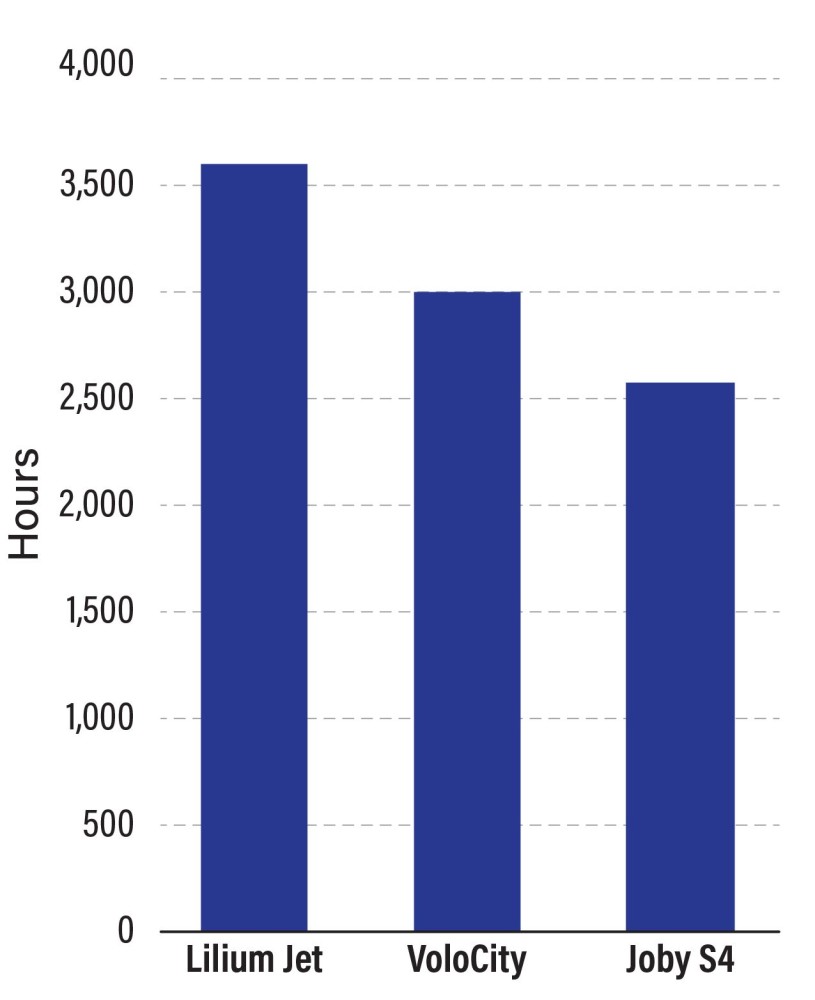

This brings us to the next questionable issue with the numbers from the leading eVTOL developers, their expected annually amount of flying hours.

They expect to fly somewhere between 2,500 and over 3,000 flying hours per year per aircraft. Compare that to current vertical flight operations, i.e. onshore helicopters fly no more than approx. 800 hours per year at best, often a lot less. Or compare to an airliner that flies much longer per flight, regional, narrow and wide body. To compare to the extreme, maybe the most utilized Boeing 737 is a -800BCF model that on average has flown approx. 3,400 hours per year with an average of 2.5 hours per flight, i.e. much MUCH longer flights than any UAM route can become, usually only some minutes long across the city and therefore has to spend time on the ground with many more turn-arounds than an airliner has to do.

Our evaluation of leading eVTOL developers numbers

Expected and budgeted 2,000 - 3,000 flight hours per year needed to create this cost per seat-mile is no where near being remotely realistic in the real world of vertical flight operations on very short passenger routes, especially on aircrafts landing and taking off primarily only used for VMC operations meaning they have to operate in good weather conditions, which it never is every single day all year around anywhere in the world, which put even further constrains on the eVTOL UAM aircrafts ability to fly the needed 2,000 - 3,000 hours per year to deliver the low enough cost per seat-mile. Not to forget their limited to no range beyond urban areas.

Operating a light helicopter used A LOT less than the leading eVTOL aircrafts prices are publishing needed to match the same approx. price per seat-mile, one has to ask; Where is the great saving for using these leading eVTOL developers aircrafts for UAM services ? - and to repeat Kevin Michaels question: ".. If there is such pent-up demand for this service, why isn’t the world covered with R44 air taxis .." - or equivalent light helicopters.

Is the disruptor becoming disrupted ?

Having documented above the Business Case of using helicopters for UAM services being tried again and again without success, having documented that the numbers set forward by the leading eVTOL developers are at best roughly at price with current UAM services using current light helicopters, at a more realistic picture to be more expensive than using current light helicopters at least when it's not scaled up and cost lowered enough to include the masses ability to afford the UAM services, we haven't even yet included in our overall assessment the upcoming disruptor we believe we shall expect to disrupt among others, these UAM designed eVTOL's:

- The Autonomous Car

As mentioned previously, using UAM services require a land-based service to bring the passenger to- and from the UAM's infrastructure, their landing locations, since UAM services can not land nor takeoff at each passengers exact addresses especially in a congested area like a city. That would also counteract the purpose of ride-sharing and not flying one passenger around in each eVTOL aircraft, there has to be a mutual collecting and delivering point in each end of the flight.

Existing Public Transportation such as metro, tramp, busses etc. can be used but has its cons for not being bespoke to the individual passenger need such as being slow to get to ones destination, inconvenient due to they have a set schedule the passenger must adapt to and different route to follow than going direct and sometimes crowded with to many people we don't feel comfortable with especially after the COVID19 trials. Taxis or an UBER or such service can be a good alternative for getting a bespoke service, but is much more costly than the other types of public transportation. Private cars are even better, but then the passenger has to think of parking issues and the cost for that and just like the taxi or UBER service, can often get stuck in congestions in the cities.

What the upcoming autonomous car will do is give the best of public transportation and private car ownership in the same package.

- Individual bespoke travel or ridesharing with just a couple of people, for example the same people you will be flying with at the regional airport or vertiport it drives you to.

- Cost effective, 4-10x cheaper than owning a car let alone even more cheaper than a taxi or an UBER service with a driver onboard.

- Much larger utilization of each car compared to owning a car, whom sits non-utilized on average 95% of its lifetime, meaning much fever cars on the road leading to less possible congestion if any.

- No parking cost nor risk of finds or wasting time finding a free parking lot.

- Quicker with no human and slow to respond driver, can drive closer together on the road using less space on the roads and still be safe.

- Safer than a human driver.

- Via a MaaS (Mobility as a Service) platform simple to use with a one-ticket system for multi-module transportation.

Then the question arises, when the Autonomous Car can bring the passenger quick, very cheap, safe and seamless to the eVTOL's helipad with maybe only 20% of the car fleet left due to the implementation of a wast majority of autonomy on the roads, what delaying congestions are we talking and comparing the future UAM services with, or maybe we shall ask where are the future congestions then if anywhere ?

What passenger who now sits comfortable in an autonomous car, having a coffee and checking emails, news, video call etc. wants to be disturbed by having to close whatever he/she is occupied with in the autonomous car, transfer from car to eVTOL with a short but mandatory security and safety briefing session, timing his/hers travel and schedule with a ride-share eVTOL's schedule and shortly later transferring back to another autonomous car to get to his/hers final destination and not saving much if any total travel time at all, instead of just staying in the first autonomous car and drive all the way to his/hers final destination while doing whatever the passenger wants to occupy their travel time with in the autonomous car ?

Are developers (aircrafts and infrastructure), investors, advocates etc. for UAM services comparing past and present data with a different future without including all the expected new differences in the future ? - because if autonomous cars are to be expected to roll out at large scale during sometime in the next decade, UAM services seems to be history before UAM has even taken off for real with Billions upon Billions of invested capital wasted along with it.

For that reason we believe Air Mobility services need to move passengers on a longer distance to make sense at all, to provide some significant value of timesaving for the passengers total travel time incl. the transfers between land and air and back again, especially in places where there is a good build-out land-based public transportation system in the cities and its urban areas and/or good road network.

We believe primarily in RAM (Regional Air Mobility), where we move the passenger a larger distance of min. 100-150 land-kilometers or more including individual geo- and topographic challenged areas where a shorter distance can be viable for RAM, and UAM will globally only be a niche in some special select places like massive metropolitans such as Singapore, New York, Los Angeles and such like. With the data in hands we do not believe UAM will be able to support thousands upon thousands of UAM designed eVTOL aircrafts, especially not for the masses with the expected ticket prices published. It is difficult to see with the data in hand that UAM will scale significantly with the autonomous car arriving, resulting in diminishing UAM's advantages significantly.

We further believe with the data we have that RAM will cost-wise be best and cost competitive in a combination where the cheaper to operate eSTOL aircrafts can be utilized and supplied with cheap-enough-to-operate eVTOL aircrafts where eSTOL aircraft nearby can not land and support the catchment area.